Last September in the post Another Reason Real Estate Prices Will Drop Further, I outlined how the banks that got burned by easy lending would be forced to tighten their lending. At the time of the post, Fannie and Freddie were moving to a 10% down payment requirement.

It has only been a few months since then and the new guidelines have gotten tougher. Much tougher. From the SF Gate article Home buyers to be dinged with new fees:

Under Fannie’s and Freddie’s new guidelines, even applicants who assumed their FICO scores would get them favorable rates will be charged more unless they can come up with down payments of 30 percent or higher. For example, a buyer with a 699 FICO score who can make a down payment of 25 percent will now get hit with a 1.5 percent “delivery” fee at closing under the new guidelines.

A buyer with a Fair Isaac Corp. FICO score between 700 and 720 will pay an extra three-quarters of a point. Even someone with a 739 FICO will get dinged with a quarter-point add-on.

30% down payment! I knew lending would move back to the 20% down model. Never did I think it would overshoot to 30% down. The point of a down payment is to protect the lender should the borrower walk away. A 20% down payment assures the lender feels some pain if they stop making payments.

With a 20% down payment, the lender has enough insurance that should they be forced to foreclose and resell the property they don’t lose money. The only reason to go beyond 20% is because the lender feels the underlying asset (the home) will drop in value as much or almost as much as the down payment.

The new guidelines tell us that Fannie and Freddie are projecting a large housing price decline.

The article continues:

Applicants who seek to buy a condominium and cannot come up with a 25 percent down payment will be hit with a three-quarter point add-on penalty, no matter how high their credit score - simply because they are not purchasing a traditional detached, stand-alone home.

First-time home buyers often purchase condos. How will they come up with a 25% down payment to avoid the penalty? Prices have to fall. Even if they assume the 3/4 point penalty, the seller will take that hit in the form of further price cuts. This will put even more condos underwater and cause more owners to walk away. This is going to crush the Downtown Miami.

What percent of home buyers will be affected by these fees? I tried to find updated FICO averages, but couldn’t. An average of sites that cited scores from 2006-2007, stated that 42% are below 700 and only 18% are above 800. In other words, the new guidelines aren’t targeted at deadbeats. They target the majority of potential home buyers. It is Fannie and Freddie’s response to lending while housing prices are in free fall.

Comments

TigerAl

February 17 at 2009 at 10:03 PM

I have to say that I disagree that the 25-30% down payment and extra fee requirements are because Fannie and Freddie are projecting a further decline. Lenders in some other countries (my sister had to do this in Australia) require a 50% down payment. It seems more to me like they are finally enforcing stricter lending standards and forcing people to have a higher stake in home purchase and ownership as well as showing that they know how to use credit wisely. It’s much harder to walk away from a home in which you have 25-30% equity.

I do agree that there will be some impact on the home prices (though not even close to as extreme as your prediction) because supply will outweigh demand with a lot of homes on the market and some buyers just unable to come up with the funds. Would you say that that is a problem? I don’t think so, it’s about time something was done about people who want what they cannot afford and make other people and businesses pay for it. For the record, I don’t buy the “bank lied to me” statement, no one put a gun to their head to make them buy anything. It’s greed, pure and simple.

MAS

February 17 at 2009 at 10:57 PM

The only reason someone walks away from 20% down is because they are in a desperate situation. Raising it to 25% or 30% changes little from a buyers ethics prospective. IMO, it is an admission by Fannie and Freddie that they see big price declines coming.

Ironically, these new guidelines will ensure that those price declines occur. Especially with condos.

When you mix huge inventories with higher than historical norm down payments, you will end up with an over correction in prices.

Is that good?

Not for the people that need to move and can’t sell their property without taking a huge loss. I sympathize with them. It only benefits renters on the sidelines with excellent credit scores and sizable savings.

TigerAl

February 17 at 2009 at 11:47 PM

If these people are selling in a depressed market and then will probably buy again in the same depressed market someplace else, are they really in a worse situation than if they had held on to their homes till the market recovers?

MAS

February 17 at 2009 at 11:59 PM

It means the person that bought a conforming loan with 5-10% down between 2003-2007 will very likely need to bring money to the table to sell their own place. Let us assume they can. Now they need to cough up 20-30% down for their next home. Most people aren’t that cash rich.

TigerAl

February 18 at 2009 at 12:48 AM

Very specific case, MAS. There are too many variables (location of homes, original loan, new loan, etc) in this equation to say that they will be worse off.

My question was a general one since as a seller in this market, they would be at a disadvantage but would have the upper hand as a buyer. They could, in fact, come out even or even better off.

MAS

February 18 at 2009 at 1:04 AM

According to ZILLOW, 41.2% of all mortgages bought in the last 5 years are now underwater. If these people want to leave their home, they need to bring cash to the closing.

So if you aren’t part of that group AND you have enough savings to put 20-30% down - then sure it balances out.

Home sellers also incur a 5-6% fee for selling, so my guess is the ZILLOW number is low. And that number is growing.

I’m not saying everyone will be worse off, but enough people will be to depress home prices at an accelerated rate.

Matt

February 18 at 2009 at 4:14 AM

Until median home prices are no higher than 3% of total household income for the given submarket, valuation is not ‘correct’. Where I live, the median home price has come down quite a bit from the 2005 prices, but it’s still way too high (~$450k). Very few people have a total household income of over $125k/yr. If you read media reports, you hear words like “free fall” or “biggest decline in decades”. All is happening is that prices are (very slowly) getting closer to ‘normal’. IMHO, we are simply seeing a pricing correction that has long been over due. Unfortunately, many good people are getting creamed in the process (I empathize with a lot of them). So, once prices get closer to ‘normal’ and the banks get back to ‘normal’ (20% down, little to no fees for strong borrowers), we will reach stabilization in the housing market. But by then, we humans will probably find something else to create a bubble with (hopefully it will be more of a sustainable, cross sector modest growth versus a bubble — ‘green collar’??).

Jim

February 18 at 2009 at 9:02 AM

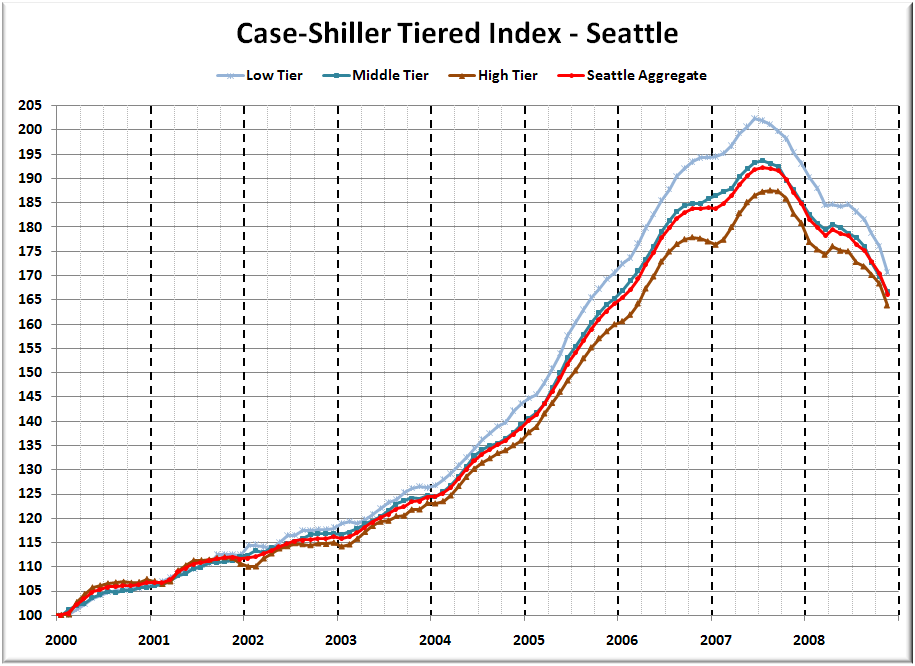

If you follow this link it will take you to the Case-Shiller Index for Seattle:

http://seattlebubble.com/blog/wp-content/uploads/2009/01/case-shiller_seatiers_2008-11.png

{kind=link}

The current level is about 165 (peak at ~ 190). If you do some calculations you will find: 80% (or 20% down) = 132 70% (or 30% down) = 115

So 20% down takes you back to about 2005.

30% down takes you back to about 2003 …which appears to be where prices first went parabolic.

It appears that the banks think we will not go lower than 2003 prices, but will go below 2005 prices. They are obviously not good at predicting such things or most would not be technically insolvent …but I think that is what they think regardless.

Finally, if you honestly don’t think this is the reason banks are suddenly demanding 30% down, then provide a better reason. No offense, but what they do in Australia is not a better reason.

Jim

February 18 at 2009 at 9:35 AM

And just as an exercise, take a look at:

- The DOW - 1929 - 1933

- The NASDAQ 1995 - 2003

- Oil - 2007 to Present

- The Case-Shiller link above.

The common thread here is that all four examples are economic bubbles that burst.

Further, the steepest monthly house price decline yet was just last month …and Seattle UE just kicked into 5th gear!

Seattle house prices are headed waaaay lower folks… sad, but true. :(

TigerAl

February 18 at 2009 at 4:39 PM

Jim, Just so you know..I am very aware of the Case-Shiller index. I have 2 statistics degrees, have done more simulations and forecasting than most people and have even worked through how the C-S is constructed. BTW, I disagree with some of the assumptions made in developing the index which I choose not to get into on this blog. Incidentally, I cited Australia as an example of countries with better lending practices and not as a reason. I don’t think anyone in their right mind disputes that stricter lending practices are needed in this country.

TigerAl

February 18 at 2009 at 5:02 PM

And here is my last comment on this topic: We are all providing opinions on the change in Freddie and Fannie requirements, and at this time there is no way to know for sure. If anyone wants to go down the data path, that would require quite a bit of causation (and not correlation!) modeling. I’m totally willing to change my opinion if provided with a conclusion that is supported by defensible data but I have not seen that from any of the information here.

Jim

February 18 at 2009 at 7:01 PM

Al -

- Either the Banks think housing prices will drop >20% more or they don’t.

- If they don’t, I would expect them to try to sell as many loans as they can to increase profit (or more likely reduce losses).

- Raising requirements to 30% down doesn’t do that.

So in your model, the banks don’t seem to be acting in their own best interest …that’s all I’m saying.

Andrew

February 18 at 2009 at 9:41 PM

I’m not sure Freddie and Fannie Mae are changing the lending standards because they predict a decline in prices, mostly because at this point, while it’s probably true, I don’t trust them to make accurate predictions anymore.

Even if it’s just an arm jerk reaction to the lax standards we had over the past few years, the effect will be the same. It will be much harder for people to come up with 30% down, so prices will need to drop for people to be able to afford the down payment on the property.

SwanSong

February 19 at 2009 at 6:12 AM

Not sure why no one has mentioned FHA. With FHA around there really isn’t a huge need to go Fannie or Freddie unless you plan to borrow more than 625k.